Graeme Dreghorn

View profileDirector

For many years, retirement income planning followed a relatively simple path. Savers built up pension pots, converted that wealth into a guaranteed income, and relied on that certainty to fund later life. Today, that landscape looks very different.

Longer life expectancies, changing pension freedoms and evolving tax rules mean retirement is no longer a single, fixed phase. Instead, phases can span several decades, with income needs, spending patterns and priorities shifting over time. Against this backdrop, flexibility has become an important consideration within retirement income planning.

People are spending more years in retirement than ever before. While this is a positive outcome of improved health and longevity, it also increases the complexity of planning for a long retirement.

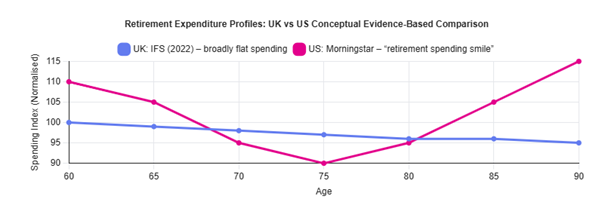

Early retirement years may involve higher discretionary spending, such as travel, hobbies or supporting family. Later years may bring different priorities, including healthcare costs or a greater preference for predictable income.

There is the commonly referenced concept known as the "retirement smile," which suggests spending peaks at the start and end of retirement with a plateau in between. This concept originates from US research . In the UK, evidence suggests spending patterns may differ, with smaller increases in healthcare costs later in life and a more gradual decline in discretionary expenditure over time.

Understanding how spending needs can change over time can help support planning approaches that are reviewed and adapted as circumstances evolve, rather than relying on decisions made years earlier that may no longer remain appropriate.

These patterns are based on population level research and will not reflect every individual circumstance.

Much of the discussion around retirement income focuses on a perceived choice between pension drawdown and guaranteed income solutions, such as annuities. In practice, retirement income planning may involve a combination of different approaches.

Drawdown can provide flexibility and control over income, allowing withdrawals to vary over time. It also involves investment risk, and income levels are not guaranteed.

A guaranteed income, such as annuities, can provide a known level of income for a set period or for life. This can help meet essential expenditure needs, but usually involves giving up access to capital and flexibility. Rather than viewing these options in isolation, some people choose to consider how different income sources might work together. This may involve securing a degree of guaranteed income to cover core spending needs while retaining some flexibility elsewhere. The most appropriate balance will always depend on individual circumstances, objectives and attitude to risk.

Retirement income decisions are increasingly shaped by the wider tax and regulatory environment. Changes to pension rules, income tax thresholds and inheritance tax treatment can all influence how retirement income and estate planning are approached.

There have been proposals and ongoing discussions around the future tax treatment of pensions, including how they may be considered for inheritance tax purposes. As with all tax legislation, this remains subject to change.

Retirement income planning increasingly interacts with wider estate planning considerations, meaning decisions about how and when income is taken should be reviewed regularly in light of personal circumstances and the prevailing rules at the time.

Market volatility is an unavoidable feature of long‑term financial planning, including in retirement - which can often span 20-30 years or more. While investment risk cannot be eliminated, it can be managed and reviewed as part of an overall strategy.

Retirement planning typically involves balancing a number of factors, including:

Holding more growth-oriented investments can increase the potential for higher long-term returns but also increases the risk of short-term volatility. Holding excessive cash may reduce volatility but can erode spending power over time. Effective planning seeks to balance these competing considerations in a way that reflects an individual’ needs and tolerance for risk.

Perhaps the most important point is that flexibility does not come from products alone. It comes from ongoing, planning and regular review.

Cashflow modelling and coordination across pensions, investments and tax considerations. As personal circumstances change - whether through markets, changes in legislation, health or family dynamics – plans may need to be adjusted to remain aligned with long-term objectives

In today’s environment, retirement planning is less about finding a single “right” answer, and more about establishing an approach that can adapt over time.

Retirement income planning has become increasingly complex – or more important. A flexible approach can help balance certainty with control, manage risk, and ensure your income strategy remains aligned with your wider financial and family goals.

Our financial planning specialists work with clients to help them consider and review income strategies that are robust, adaptable and future‑focused. If you would like to review your retirement income plans, or discuss your options, please get in touch.

Important Information

Director